Equuscorp v Glengallan Investments

Equuscorp Pty Ltd v Glengallan Investments Pty Ltd

[2004] HCA 55; (2004) 218 CLR 471 (High Court of Australia)

Case details

Court

High Court of Australia

Citations

Equuscorp Pty Ltd v Glengallan Investments Pty Ltd

[2004] HCA 55 ➤

(2004) 218 CLR 471

(2004) 79 ALJR 206

(2004) 211 ALR 101

(2004) 57 ATR 556

Judges

Gleeson CJ

McHugh J

Kirby J

Hayne J

Callinan J

Appeal from

Supreme Court of Queensland (Court of Appeal)

Equuscorp P/L & Anor v Glengallan Investments P/L [2002] QCA 380 ➤

27 September 2002

Judges

Williams JA

Mackenzie J

Chesterman J

Trial

Supreme Court of Queensland

Equuscorp Pty Ltd & Anor v Glengallan Investments Pty Ltd & Ors [2001] QSC 464 ➤

Trial Judge

Justice Helman

Issues

Terms

Parol Evidence Rule

Overview

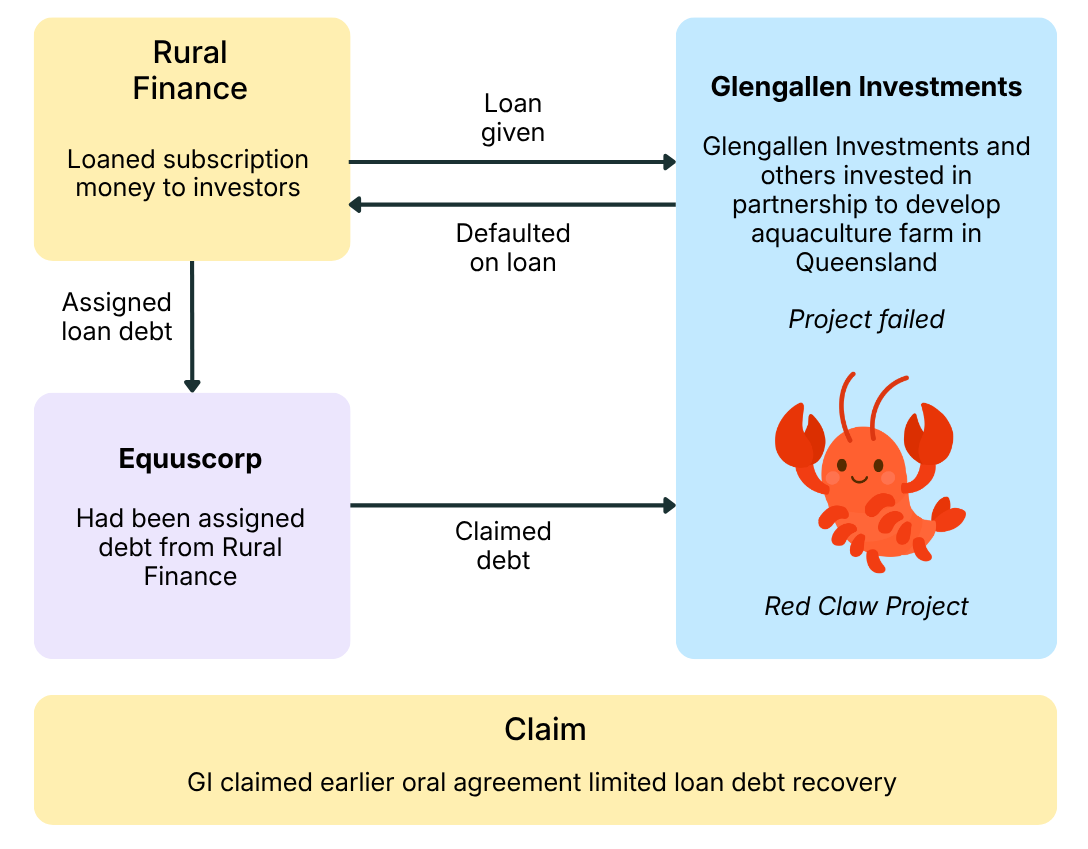

Facts

Glengallan Investments (GI) and others invested in a partnership to develop and operate an aquaculture farm in Queensland (the Red Claw Project). Some of them, including GI, obtained loans from Rural Finance (a lender related to the investors). The project later failed and GI defaulted. Rural Finance assigned the loan debt to Equuscorp and Equuscorp claimed the debt from GI.

The claim

GI claimed there was an earlier oral agreement that limited what could be recovered.

They also claimed the whole arrangement was a sham.

The trial judge

Justice Helman held that the terms included the earlier oral terms which limited recourse on the loan.

His Honour further held that the arrangement was merely a charade; no loans had been made.

On appeal to Queensland Supreme Court (Court of Appeal)

Did not agree with Justice Helman that the oral terms applied - the contract was governed by the written loan agreement. Nevertheless, agreed that it was a sham - no loans had been made.

On appeal to High Court

There was a written loan agreement which each investor was bound to unless they could rely on a claim of non est factum or rectification. That was not alleged here. The alleged oral terms did not form part of the contract.

None of the transactions were a sham.

Appeal allowed

High Court of Australia

The Court (on the question of oral terms)

[Their Honours set out the essence of each of the appellants’ and respondents’ case as follows]

The appellants' case in the courts below

[15] The appellants' case against the respondents was simple. They alleged that on 30 June 1989, Rural Finance made written loan agreements with each respondent. By each of those agreements, Rural Finance agreed to lend, and the relevant respondent agreed to borrow, a sum which the borrower directed the lender to apply "in payment of the Application Moneys [for units] and otherwise in accordance with the Borrower's obligations under the [Partnership] Deed". The appellants alleged that Rural Finance had done this but that each respondent had defaulted in the repayments of principal and interest.

The respondents' case in the courts below

[16] The respondents' case was much more complex. First, they alleged that the loan agreements were made in June 1989 but were wholly oral. Each was said to be constituted by a number of conversations taking place between early June 1989 and 30 June 1989 "but prior to the execution of the Loan Agreement" (emphasis added). The respondents alleged that it was a term of these agreements (referred to in the pleadings as the "operative agreement[s]") that the liability of each respondent was limited. It was said that liability was limited to one payment on 30 June 1989 and two subsequent payments on 30 September 1989 and 31 December 1989, and that, thereafter, "the income generated by the limited partnership would be applied in extinguishment of the balance of the ... loan". It is convenient to refer to this allegation of limited liability as the "limited recourse" point.

[17] The primary judge held [[2001] QSC 464 at [15]] that the respondents should succeed on the limited recourse point. He accepted the oral evidence given by certain witnesses for the respondents about the conversations on which they relied and concluded that the operative agreements alleged by the respondents governed the relations between the parties. On appeal, however, it was held [[2002] QCA 380 at [89]] that the finding that the terms of the loan were agreed upon orally could not stand.

[18] The second argument advanced by the respondents was that Rural Finance had not provided a cheque, or paid cash, to Eagle Star for the units and, therefore, had not made the alleged loan to the respondents. This may be called the "real money" point and on this point the respondents succeeded both at trial and in the Court of Appeal.

[19] Thirdly, the respondents alleged that they had entered the operative agreements and subsequently signed the written loan agreements relying on representations: (a) that the liability of the respondents was limited in the manner described earlier; and (b) that Rural Finance "had sufficient funds to lend" to the respondents by way of a payment to enable the respondents to acquire the relevant number of units in the limited partnership. Each of these representations was said to be misleading … Neither the trial judge nor the Court of Appeal found it necessary to decide any of them.

[20] Finally, the respondents alleged that the purported assignments by Rural Finance to Equuscorp of the respondents' debts were ineffective either because the respondents were not indebted, or because the assignments were conditional, and failed for want of fulfilment of the conditions. [This claim did not arise on appeal]

…

Written agreements or oral?

[31] Debate in the courts below, about whether the loan agreements were wholly oral, as the respondents alleged, or wholly written, as Equuscorp and Rural Finance contended, proceeded upon the premise that the critical question was whether the primary judge should have acted on his acceptance of oral evidence given on the respondents' behalf of some conversations that were said to have occurred before the written loan agreements were signed. That, in turn, was seen as a question to be decided by reference to whether subsequent events (including those we have mentioned) made it more or less probable that during these conversations some consensus was reached that the loans were "limited recourse". But behind these arguments lies a more fundamental issue which the respondents' contentions did not address, whether in the courts below or on appeal to this Court.

[32] It is, and always has been, common ground that each of the respondents executed a written loan agreement on 30 June 1989. The respondents alleged that the "operative agreement" was not contained in that writing. It was said that the relevant agreement was reached earlier and was wholly oral. Yet it was not said that the written agreement should be rectified. It was not said that a defence of non est factum was available. It was not said that the written agreement was executed by mistake, or that its execution was procured by misrepresentation as to its contents or effect. (The misrepresentation alleged was as to what had been said in the conversations, not what the document was or provided.) [emphasis added]

[33] The respondents each having executed a loan agreement, each is bound by it. Having executed the document, and not having been induced to do so by fraud, mistake, or misrepresentation, the respondents cannot now be heard to say that they are not bound by the agreement recorded in it [L'Estrange v Graucob Ltd [1934] 2 KB 394]. The parol evidence rule [Hoyt's Pty Ltd v Spencer (1919) 27 CLR 133], the limited operation of the defence of non est factum [Petelin v Cullen (1975) 132 CLR 355] and the development of the equitable remedy of rectification [Taylor v Johnson (1983) 151 CLR 422], all proceed from the premise that a party executing a written agreement is bound by it. Yet fundamental to the respondents' case that the operative agreements between the parties were wholly oral, and reached earlier than the execution of the written agreements, was the proposition that the written agreements subsequently executed not only may be ignored, they must be. That is not so. Having executed the agreement, each respondent is bound by it unless able to rely on a defence of non est factum, or able to have it rectified. The respondents attempted neither. [emphasis added]

[34] There are reasons why the law adopts this position. First, it accords with the "general test of objectivity [that] is of pervasive influence in the law of contract" [Australian Broadcasting Corporation v XIVth Commonwealth Games Ltd (1988) 18 NSWLR 540 at 549 per Gleeson CJ]. The legal rights and obligations of the parties turn upon what their words and conduct would be reasonably understood to convey, not upon actual beliefs or intentions [Gissing v Gissing [1971] AC 886 at 906 per Lord Diplock; Ashington Piggeries Ltd v Christopher Hill Ltd [1972] AC 441 at 502 per Lord Diplock].

[35] Secondly, in the nature of things, oral agreements will sometimes be disputable. Resolving such disputation is commonly difficult, time‑consuming, expensive and problematic. Where parties enter into a written agreement, the Court will generally hold them to the obligations which they have assumed by that agreement. At least, it will do so unless relief is afforded by the operation of statute or some other legal or equitable principle applicable to the case. Different questions may arise where the execution of the written agreement is contested; but that is not the case here. In a time of growing international trade with parties in legal systems having the same or even stronger deference to the obligations of written agreements (and frequently communicating in different languages and from the standpoint of different cultures) this is not a time to ignore the rules of the common law upholding obligations undertaken in written agreements. It is a time to maintain those rules. They are not unbending. They allow for exceptions. But the exceptions must be proved according to established categories. The obligations of written agreements between parties cannot simply be ignored or brushed aside. [emphasis added]

[36] The conclusion that the respondents are bound by the written loan agreements may leave open the possibility that an earlier consensus reached by the parties was in each case a collateral agreement (made in consideration of the parties later executing the written agreement [Hoyt's Pty Ltd v Spencer (1919) 27 CLR 133; De Lassalle v Guildford [1901] 2 KB 215], but that has never been the respondents' case. In another case it may leave open the possibility that the contract is partly oral and partly in writing [Maybury v Atlantic Union Oil Co Ltd (1953) 89 CLR 507 at 517]. But that cannot be so here. The oral limited recourse terms alleged by the respondents contradict the terms of the written loan agreement. If there was an earlier, oral, consensus, it was discharged and the parties' agreement recorded in the writing they executed [Gordon v Macgregor (1909) 8 CLR 316 at 322‑323; Masters v Cameron (1954) 91 CLR 353 at 360‑361]. It is the written loan agreement which governed the relationship between Rural Finance and each respondent. [emphasis added]

[Their Honours found that for these reasons the ‘limited resource’ claims failed. They went on to find that the ‘real money point’ (essentially that it was a sham) also failed; their Honours remitted claims about misrepresentation and misleading or deceptive conduct for further consideration at first instance [para 60]].